Market Insights: Tuesday, September 2nd, 2025

Market Overview

Stocks opened September on a sour note, tumbling across the board as rising Treasury yields and fresh political uncertainty weighed on investor sentiment. The Dow fell about 250 points, or 0.6%, while the S&P 500 lost 0.74%, marking its worst session in over a month. The Nasdaq dropped 0.82%, leading the tech sector lower in what is historically the weakest month for equities. Wall Street began the holiday-shortened week already on edge ahead of Friday’s pivotal jobs report, and those jitters were amplified by legal drama around former President Trump’s tariffs and concerns over Fed independence. Treasury yields surged, with the 30-year nearing the critical 5% mark for the first time since July, adding pressure to equities. Meanwhile, Nvidia dropped sharply after pushing back on claims its AI chips were sold out, fueling doubts about supply-demand dynamics in the chip sector. Despite the early weakness, stocks finished off their lows as bargain hunters emerged late in the session. Still, the tone has shifted, and with economic data rolling out all week, investors appear braced for increased volatility and potential repricing of Fed policy expectations.

SPY Performance

SPY dropped 0.74% to close at $640.27 after opening at $637.50 and briefly attempting to rebound mid-session. It reached a high of $640.49 before slipping back near the lower end of its intraday range. The ETF hit a low of $634.92 before dip buyers stepped in, helping it recover somewhat into the close. Volume spiked to 70.82 million, well above average, indicating strong selling interest even as bulls worked to stabilize price. SPY finished beneath key support-turned-resistance levels, signaling that near-term momentum has turned cautious even as the broader uptrend remains intact.

Major Indices Performance

The Nasdaq led Tuesday’s decline with a 0.82% drop, followed closely by the Russell 2000 and S&P 500, both shedding around 0.55% to 0.74%. The Dow fared slightly better but still ended the day down 0.55%. A stronger-than-expected PMI failed to provide support as headlines surrounding trade uncertainty and the political tug-of-war over the Federal Reserve added to unease. Sectors with high sensitivity to interest rates, like tech, were hit hardest, while defensive names showed relative resilience. With yields rising and macro risks climbing, markets saw broad-based risk aversion take hold to kick off the new month.

Notable Stock Movements

It was a broadly red session for the Magnificent Seven, with all names ending lower except Netflix, which eked out a modest 0.49% gain. Nvidia was the weakest of the group, falling roughly 2% after management denied rumors of AI chip shortages but failed to convince investors the demand-supply balance remains healthy. Amazon and Nvidia both lost over 1.6%, continuing their recent pullbacks. The group’s collective weakness contributed significantly to market losses, reinforcing concerns that stretched valuations and slowing momentum in market-leading names could weigh on broader indices if selling continues.

Commodity and Cryptocurrency Updates

Crude oil defied broader market weakness, surging 2.42% to $65.56, though our model continues to anticipate a pullback toward $60 over the coming months as global demand softens. Gold jumped 2.37% to close at $3,599, reaching levels not seen since spring as investors sought safety amid rising political and rate cut uncertainty. Bitcoin also rallied, gaining 2.27% to close above $111,300, bouncing back from recent weakness and following the broader risk-on move seen late in the session.

Treasury Yield Information

Yields climbed across the curve, with the 10-year Treasury closing at 4.275%, up 0.68% on the day. The move reflected rising doubts about the Fed's path and heightened political risk, including ongoing trade tensions and questions about central bank independence. The 30-year yield's approach toward the 5% threshold, a historically critical level, spooked equity investors. While still below danger territory, yields approaching 4.5% to 4.8% could increase downside pressure on stocks, particularly growth names. With markets now fixated on Friday’s jobs report, yields will remain in focus.

Previous Day’s Forecast Analysis

Friday’s newsletter called for SPY to trade between $640 and $650 with a bearish bias, emphasizing that weakness below $645 would open the door to further downside with targets at $640, $637, and $635. Resistance was identified at $648, $650, and $652, while bulls were expected to defend $643 overnight. The strategy leaned short beneath $645 with the potential for limited upside if buyers reclaimed $648. The VIX had climbed to 15.36, signaling rising risk and supporting a defensive posture. The analysis highlighted September seasonality and softening momentum as risks for bulls heading into the week.

Market Performance vs. Forecast

Tuesday’s market closely aligned with Friday’s bearish forecast. SPY gapped lower at the open, beginning at $637.50, well beneath the $645 threshold, and quickly tested downside targets with a low of $634.92. The projected range of $640 to $650 proved too high, with SPY closing at $640.27 just under the expected lower boundary. Key support levels including $640 and $637 were tested, and while $635 narrowly held, momentum clearly favored the bears. The model's call for limited upside and likely rejection of rallies held true, and traders who executed shorts beneath $645 likely found solid entries with profits available at multiple downside targets. Once again, the analysis provided clear, actionable levels for intraday planning.

Premarket Analysis Summary

In Tuesday’s premarket analysis posted at 6:54 AM, SPY was trading at $640.41, and the model identified 641.20 as the bias level with upside targets at $643.20 and $644.70. On the downside, key targets included $640, $638.70, and $633. The model leaned toward upward consolidation but warned of a potential selloff to $633 if support failed. It suggested the most likely scenario was a rally attempt from lower levels with limited upside, while acknowledging sellers could regain control. The session was expected to feature two-way action and emphasized the importance of trading reactively around key inflection points.

Validation of the Analysis

Tuesday’s action validated the premarket analysis with high accuracy. SPY opened sharply lower, quickly testing downside levels as forecast. The market dipped through $640 and touched $634.92, just shy of the lower end of the projected range. While the model had anticipated some rebound off lower levels, resistance at $641.20 held and upside was capped near $640.49. The forecast’s expectation of upward consolidation off lower targets played out briefly, but sustained selling ultimately confirmed the premarket's more cautious lean. Traders following the premarket plan had clear levels to trade around, particularly the move from sub-$640 to $638 and the test of $635, reinforcing the reliability of the model's real-time analysis.

Looking Ahead

Wednesday’s session brings the JOLTS Job Openings report, a closely watched metric that could give markets another data point on labor market strength ahead of Friday’s critical Nonfarm Payrolls release. With rate cut expectations fluctuating and political risk re-entering the picture, traders should prepare for heightened volatility. JOLTS data can move yields, especially if it surprises to the upside or downside. Combined with current technical weakness and rising VIX, tomorrow’s report could serve as a catalyst for SPY to either stabilize above key support or extend losses further. Stay nimble.

Market Sentiment and Key Levels

SPY closed at $640.27, sitting just below the key support-turned-resistance level of $643, suggesting sentiment has shifted cautiously bearish in the short term. Bulls must defend $638 overnight to prevent a retest of Tuesday’s lows at $635 and potentially $630. Below $630, support thins rapidly, and losses could accelerate toward $625. On the upside, reclaiming $643 would open a path toward $645 and $647, but bulls face a tough climb amid rising volatility and weakening leadership from major tech stocks. Overall, the uptrend remains intact, but momentum is fading, and the battle at $638 will be critical in determining near-term direction.

Expected Price Action

Our AI model projects SPY to trade between $634 and $645 on Wednesday, a wide range that suggests trending price action is likely with sharp reversals possible. The bias remains bearish, as the Put side continues to dominate positioning. If SPY breaks below $635, expect sellers to press toward $630, with further risk of downside acceleration to $625. Conversely, a move above $643 could trigger a short-covering rally toward $645 and $647, though momentum would likely stall near resistance unless fueled by a surprise JOLTS report. Actionable intelligence suggests leaning short below $640 and looking to fade rallies into resistance, while respecting volatility and the potential for failed breakdowns near $635. The setup favors active, flexible trading with a defensive posture as macro uncertainty looms.

Trading Strategy

Traders should favor short setups below $640 with targets at $637, $635, and potentially $630 if downside momentum persists. A clean break below $635 could invite acceleration toward $625, but tight stops are advised as reversals may be fast. Long setups can be considered if SPY reclaims $643 with strength, offering upside targets at $645 and $647. However, upside remains limited unless bulls gain traction above $648. With the VIX now at 17.18, up 6.58% on the day, volatility is increasing and caution is warranted. Position sizes should be trimmed, stops should be tightened near key levels, and overnight holds should be limited. Be ready for whipsaws around economic releases, and maintain a flexible approach that favors trend-following strategies in the direction of breakout moves.

Model’s Projected Range

SPY’s projected range for Wednesday sits between $633.50 and $646.75, with the Put side dominating in a narrowing band that suggests periods of trending price action with intermittent chop. A stronger-than-expected PMI did little to lift markets as concerns about tariffs and White House policy adjustments to counter court decisions weighed heavily. While sideways action was anticipated, we also warned that macro risks loomed large and to always be prepared to trade what you see. Friday’s jobs report remains the key event of the week, with the potential to materially move markets. On Tuesday, SPY sold off more than 1.4% before dip buyers stepped in, closing the day down 0.73% at $640.29, well off the lows of $634.92 after a large gap down and sustained selling at the open. Still, the damage has been done, and the bears are out of hibernation, at least temporarily, as higher-than-average volume suggests further weakness ahead. We cautioned last Friday that once $643 failed, near-term trend risk tilted lower even as bulls retained control of the broader structure. For Wednesday, with little economic data due, absent a catalyst the bulls want to defend $638 overnight; failure to do so would open the door to today’s lows at $635 and potentially $630, where a breakdown could accelerate losses toward $625 with limited support below. If bulls can hold $638, however, they will attempt to repair Tuesday’s damage and seek a close above $645 as a step toward prior highs. As we have said for over a week, $660 remains necessary to confirm the breakout, and failure to reach it would suggest a near-term top, especially given September’s reputation for negative returns. With Wednesday’s narrowing range, two-way trading is favored. Resistance is expected at $643, $645, $647, and $649, while support lies at $638, $636, $635, and $630. Since reclaiming $585, SPY has remained in a steady uptrend supported by dip buyers, but today all Mag stocks lost ground except Netflix, with leaders like Nvidia and Amazon shedding over 1.6%. For two weeks we have warned that continued weakness in these leaders would drag the broader market lower, as the parabolic advance carries rising risk with limited reward. We also noted Thursday that our model was flashing early signs of weakness after the first week of September, and that warning may be arriving ahead of schedule; as such, quick profit-taking and caution with overnight holds are advised. The VIX jumped 6.58% to 17.18, and while September often sees VIX near 20, contango in VXX futures suggests volatility may actually decline. Still, we lean toward VIX 20 arriving this month, though perhaps not this week. If you haven’t yet added protection to your long book, now is the time, given the coin-toss scenario shaping up for September. VIX below 23 reinforces the bullish case, but a breakout above that level could finally spark the long-anticipated 5–10% pullback. SPY closed well below the bull trend channel from the April lows, which should be taken as a warning sign; while the model did not redraw the channel after just one day, if price remains below the bullish channel for more than three days, the model will certainly reset this steep, uncorrected bull channel.

Market State Indicator (MSI) Forecast

Current Market State Overview:

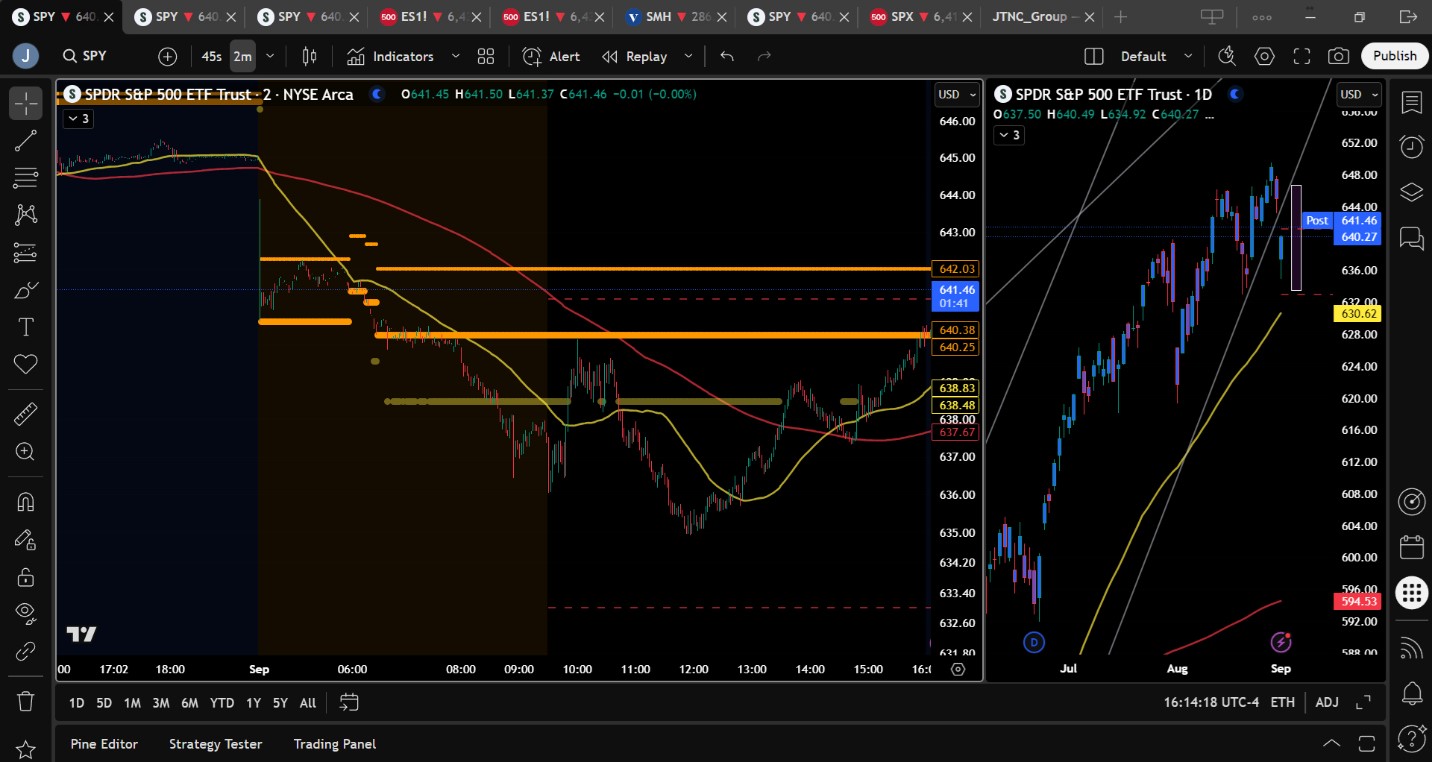

The MSI ended the day in a narrow Bearish Trending Market State, with SPY closing just above MSI support. While no extended targets were present at the close, they printed through much of the session as SPY failed to hold $643 overnight, prompting several MSI rescalings lower in the premarket. By the open, the MSI had settled into a range with extended targets below, signaling herd participation in the day’s decline, though the lack of continued rescaling lower suggested the trend was not as weak as it appeared. That proved correct as dip buyers stepped in at major support near $635, reversing the market to close above its open and pushing SPY back toward reclaiming $645. The current MSI implies some risk of a retest of today’s lows overnight or into Wednesday, but absent an external catalyst, we expect dips to be bought. MSI resistance stands at $642.03, with support at $640.38.

Key Levels and Market Movements:

On Friday we wrote, “traders should also be wary of any external news out of the White House that could jolt price action,” and noted, “the session is likely to deliver more sideways, two-way trade with some follow-through from today’s decline,” while also stating, “The broader structure continues to favor the bulls until major support levels are lost, so we maintain a preference for long setups above $640 while remaining open to shorts on a confirmed break below that level or on a failed breakout above $645.” With that context, and with the MSI opening in a Bearish Trending Market State with extended targets below, we waited for a retest of MSI support-turned-resistance at $640 to go short on a clean failed breakout. Without an MSI target below, we turned to the premarket and set T1 at $638.70, which was reached quickly. Extended targets began printing again, so we set T2 at the next premarket level of $633, which felt like a stretch. But as always, we trade our levels or our highest-probability patterns. Sure enough, at the day’s lows SPY formed a textbook failed breakdown at $635.50, so we exited our short but did not flip long immediately given extended targets were still printing. By the time the herd stepped aside, price had rebounded to $639, leaving little to lean on but the premarket level of $638.70. We waited for extended targets to stop printing and, on a pullback to $637.75, entered long just below $638.70 with T1 set at MSI support-turned-resistance at $640.25. With less than five minutes left in the session, we took off the trade at T1, closing the day with a solid countertrend long after a monster short. Two for two and a great way to start the week, thanks to a clear plan, disciplined execution, and strong alignment between MSI signals, our broader market model, and key technical levels. The MSI continues to be a cornerstone of our consistent trading process.

Trading Strategy Based on MSI:

Wednesday brings the JOLTS Jobs report, but with the monthly jobs report due Friday, it is unlikely to materially move markets. While the market may trend, it is more likely to drift into Friday’s release, with traders needing to stay alert for any external macro events that could jolt price action. Absent a catalyst, Wednesday is expected to deliver more sideways, two-way trading as the market looks to build on today’s dip-buying off the lows. The bulls want to reclaim $645 to push SPY toward new all-time highs, while failure to do so would open the door for bears to retest today’s $635 low, a level we have noted for some time as critical for bears to break to generate momentum. They failed to break it today, leaving bulls in control of the broader narrative…for now. Our bias remains to favor buys on a retest of today’s lows while also considering short setups on failed breakouts near current levels and until $645 is reclaimed. Overall, we expect the market to retest today’s lows to reveal how much strength the bulls have left. As always, failed moves remain among the highest-probability setups. Stay nimble, avoid trades during Ranging Market States, and ensure full alignment with MSI. Providing real-time insights into market control, momentum shifts, and actionable levels, the MSI when integrated with our Pre-Market and Post-Market Reports continues to sharpen execution precision and elevate trade quality. If you haven’t yet integrated MSI and our model levels into your process, now is the time. Contact your representative to get started as these tools are designed to support consistency and enhance performance.

Dealer Positioning Analysis

Summary of Current Dealer Positioning:

Dealers are selling SPY $645 to $660 and higher strike Calls while also buying $641 to $644 Calls indicating the Dealers desire to participate in any relief rally on Wednesday. The ceiling for Wednesday appears to be $645. To the downside, Dealers are buying $640 to $595 and lower strike Puts in a 3:1 ratio to the Calls they’re selling/buying displaying a less concern that prices could move lower on Wednesday. Dealer positioning has changed from bearish to slightly bearish/neutral.

Looking Ahead to Friday:

Dealers are selling SPY $645 to $670 and higher strike Calls while also buying $641 to $644 Calls indicating the Dealers desire to participate in any rally this week. The ceiling for the week is likely $650. To the downside, Dealers are buying $640 to $540 and lower strike Puts in a 5:1 ratio to the Calls they’re selling/buying, reflecting an bearish outlook for the week but one which has abated somewhat. For the week Dealer positioning has changed from strongly bearish to bearish. We advise reviewing Dealer positioning daily for directional clues. These positions evolve quickly and tracking them is essential for staying ahead of shifting market sentiment.

Recommendation for Traders

SPY finished Tuesday at $640.27 following early weakness and a midday recovery that ultimately failed to reclaim major resistance. Traders should favor short setups below $640 with targets at $637, $635, and potentially $630. Longs are viable above $643 with upside capped near $647. Volatility remains elevated with the VIX at 17.18, and broader market sentiment is shifting cautiously bearish. Manage position size carefully, use tight stops in both directions, and avoid aggressive exposure without confirmation. Be ready to flip bias if key levels break. As always, review the premarket analysis posted before 9 AM ET to account for any changes in our model’s outlook and in Dealer Positioning.

Good luck and good trading!